One medical testing company was led by a convicted felon, another was accused of delays and unreliable results

Like many states, Florida has worked hard to quickly ramp up diagnostic testing for SARS-CoV-2, the coronavirus that causes the COVID-19 illness. For the most part this has been a good thing. However, local media in that state reported problems with two no-bid contracts for clinical laboratory testing, including one with a Dallas-based company whose founder pleaded guilty last year to two felonies involving insurance fraud.

In a press conference announcing the two deals, Florida Governor Ron DeSantis said, “We have two contracts in place with two new labs that will increase our lab capacity by 18,000 samples per day.” He added that he expected a 24- to 48-hour turnaround.

“That’s a lot better than we’ve been getting from Quest and LabCorp,” he said. “These labs will be primarily where we send our samples that we collect in the long-term-care and assisted-living facilities and at the community-based walk-up sites.”

The announcement followed DeSantis’ March 9 emergency decree, which allowed state agencies to award contracts to companies without undergoing formal bidding processes, reported Florida Bulldog, an independent non-profit news site.

In his announcement, DeSantis did not identify the companies that had received the lab test contracts. However, Florida Bulldog reported that those companies were:

Indur Services, a Dallas-based health-coaching company, and

Southwest Regional PCR, a CAP-accredited lab in Lubbock, Texas, that does business as MicroGenDX Laboratory (MicroGen Diagnostics, LLC).

The Indur contract—initially valued at $11.3 million—included $10.2 million for 140,000 COVID-19 RT-qPCR test kits, plus additional payment for supplies, Florida Bulldog reported based on information from the state contract database. Later, the contract was reduced to $2.2 million solely for supplies.

The MicroGenDX contract—valued at $11 million—called for 8,000 tests per day for 14 days at a cost of $99 per test, Florida Bulldog reported. That contract was later cancelled due to concerns about reliability and processing speed.

Indur’s Legal Troubles

Indur is a self-described “health and wellness lifestyle and products company” founded in 2017 by Brandt Beal, according to Business Insider. In 2019, Beal pleaded guilty to two felonies involving insurance fraud in Texas and was given 10 years’ probation in each case, Florida Bulldog reported. He also was required to pay restitution. He pleaded guilty to a separate charge of felony theft in 2017 and was sentenced to nine years’ probation.

In an interview with Florida Bulldog, Beal claimed that “the man who pleaded guilty to those charges is actually his cousin with the same name.” However, Beal “would not provide requested contact information for his cousin,” the Florida Bulldog reported, which posted photos demonstrating that the Indur founder and the person who pleaded guilty to the felonies were the same individual.

Jason Mahon, Communications Director at the Florida Division of Emergency Management (above), told Florida Bulldog that Indur’s COVID-19 testing contract was scaled back in May “because Indur Services did not provide testing directly, but rather was providing testing services through another company.” The state then contracted directly with that clinical laboratory company to obtain the COVID-19 testing services. “Time is of the essence when securing these critical testing supplies for Floridians, and that limited time does not allow for the Division to vet every company’s executive leadership or board of directors,” Mahon told Florida Bulldog. (Photo copyright: LinkedIn.)

The amended contract, valued at $2.2 million, called for Indur to deliver swabs and vials. “To date, everything that’s been ordered they’ve delivered on,” said Jared Moskowitz, Director of the Florida Division of Emergency Management department.

Testing Delays Snag MicroGen Diagnostics

The state cancelled its contract with MicroGenDX on May 15, Florida Bulldog reported.

“As with any lab, we do our due diligence to ensure the company will be able to provide reliable services before sending any samples,” said Jason Mahon, Communications Director at the Florida Division of Emergency Management. “Upon further interaction with this vendor, the Division determined that the state could not be 100% confident in the results that would come from this vendor, or with the processing speed, which is critical for COVID-19 testing.”

This came as AdventHealth, a non-profit health system based in Altamonte Springs, Fla., was having its own difficulties with MicroGenDX.

On May 16, AdventHealth announced that it had terminated a COVID-19 testing contract with an unnamed third-party lab, claiming that the provider was “unable to fulfill its obligation.” Multiple media outlets later revealed MicroGenDX as the third-party lab, and USA Today reported that the FDA had launched an investigation.

“This issue impacts more than 25,000 people throughout Central Florida,” stated an AdventHealth press release. “This situation has created unacceptable delays and we do not have confidence in the reliability of the tests.” AdventHealth said it would contact affected individuals about the need for retesting.

However, MicroGenDX CEO Rick Martin refuted the health system’s claims. “You can go after me because I didn’t meet your capacity and I couldn’t deliver on your drive-through testing because of things that I couldn’t control, but don’t attack the reliability of my test,” he told the Orlando Sentinel.

According to MicroGenDX, the company received an emergency use authorization (EUA) from the FDA on April 23 for an internally-developed RT-PCR test that can be performed on nasal swabs or sputum samples, noted a press release. The tests are run in the company’s lab facility in Lubbock, Texas.

One factor in the dispute was the handling of patient samples, USA Today reported. Martin told reporters that representatives from AdventHealth had visited the lab and observed samples that were stored at room temperature. “[Martin] maintains the samples were still valid and that the delays were due to AdventHealth not providing proper patient data and the lab running out of plastic parts used in its equipment,” noted USA Today.

Mahon told Florida Bulldog that the state did not send samples to MicroGenDX for processing. And the Florida Bulldog reported that Martin said his lab was so “hammered with huge volumes of samples” that he would have turned down any requests, adding that Martin “stood by the reliability and accuracy of his firm’s testing and said he looks forward to a day of vindication after federal inspectors conduct any inquiries.”

Collectively, these news stories scratch the surface of a bigger situation involving COVID-19 laboratory testing. The fact that Congress authorized billions of dollars to fund COVID-19 testing was noticed by some individuals who saw the funding as an opportunity to “make a quick buck” if they could get contracts to provide COVID-19 testing—whether they owned a CLIA-certified complex laboratory or not.

Thus, it’s no surprise that more companies are bidding on COVID-19 testing contracts. What remains unknown is how many of those companies are actively soliciting COVID-19 testing contracts throughout the United States.

Given this situation, and the facts recounted above, it is reasonable to ask an obvious question: Why did Florida state officials not do a more rigorous check into the credentials of the clinical laboratory entities they were preparing to award no-competitive-bid contracts to for COVID-19 testing?

Questions remain, however, over how much of the funding will actually reach hospital and health system clinical laboratories

For many cash-strapped clinical laboratories in America, the second round of stimulus funds cannot come soon enough. Thus, lab leaders are encouraged by news that Congress’ $484-billion Paycheck Protection Program and Healthcare Enhancement Act (H.R.266) includes almost $11 billion that will go to states for COVID-19 testing. But how much of that funding will reach the nation’s hospital and health system clinical laboratories?

The Department of Health and Human Services (HHS) announced the new influx of money to the states on May 18. In a news release outlining the initiative, the HHS said the Centers for Disease Control and Prevention (CDC) will deliver $10.25 billion to states, territories, and local jurisdictions to expand testing capacity and testing-related activities.

To qualify for the additional funding, governors or “designee of each State, locality, territory, tribe, or tribal organization receiving funds” must submit to HHS its plan for COVID-19 testing, including goals for the remainder of calendar year 2020, to include:

“Number of tests needed, month-by-month to include diagnostic, serological, and other tests, as appropriate;

“Month-by-month estimates of laboratory and testing capacity, including related to workforce, equipment and supplies, and available tests;

“Description of how the resources will be used for testing, including easing any COVID-19 community mitigation policies.”

“As the nation cautiously begins the phased approach to reopening, this considerable investment in expanding both testing and contact tracing capacity for states, localities, territories, and tribal communities is essential,” said CDC Director Robert R. Redfield, MD, in the HHS statement. “Readily accessible testing is a critical component of a four-pronged public health strategy—including rigorous contact tracing, isolation of confirmed cases, and quarantine.” (Photo copyright: Center for Disease Control and Prevention.)

Funding Should Go Directly to Clinical Laboratories, Says ACLA

The American Clinical Laboratory Association (ACLA), argues the funding needs to go directly to clinical laboratories to help offset the “significant investments” labs have made to ramp up testing capacity during the pandemic.

“Direct federal funding for laboratories performing COVID-19 testing is critical to meet the continued demand for testing,” ACLA President Julie Khani, MPA, said in a statement. “Across the country, laboratories have made significant investments to expand capacity, including purchasing new platforms, retraining staff, and managing the skyrocketing cost of supplies. To continue to make these investments and expand patient access to high-quality testing in every community, laboratories will need designated resources. Without sustainable funding, we cannot achieve sustainable testing.”

Some States Are Increasing Testing, While Others Are Not

Since the first cases of COVID-19 were reported in January, the United States has slowly but significantly ramped up testing capacity. As reported in the Washington Post, states such as Georgia, Oklahoma, and Utah are encouraging residents to get tested even if they are not experiencing coronavirus symptoms. But other states have maintained more restrictive testing policies, even as their testing capacity has increased.

“A lot of states put in very, very restrictive testing policies … because they didn’t have any tests. And they’ve either not relaxed those or the word is not getting out,” Ashish Jha, MD, MPA, Director of the Harvard Global Health Institute, told the Washington Post. “We want to be at a point where everybody who has mild symptoms is tested. That is critical. That is still not happening in a lot of places.”

Meanwhile, Quest Diagnostics and LabCorp continue to expand their diagnostic and antibody testing capabilities.

On May 18, Quest announced it had performed approximately 2.15 million COVID-19 molecular diagnostic tests since March 9 and had a diagnostic capability of 70,000 test each day. The company said it expected to have the capacity to perform 100,000 tests a day in June.

LabCorp’s website lists its molecular test capacity at more than 75,000 tests per day as of May 22, with a capacity for conducting at least 200,000 antibody tests per day. Unlike molecular testing that detects the presence of the SARS-CoV-2 coronavirus, antibody tests detect proteins produced by the body in response to a COVID-19 infection.

As states reopen, and hospitals and healthcare systems resume elective surgeries and routine office visits, clinical laboratories and anatomic pathology groups should begin to see a return to normal specimen flow. Nonetheless, the federal government should continue to compensate laboratories performing COVID-19 testing for the added costs associated with meeting the ongoing and growing demand.

Report’s authors claim the US needs to be testing 20-million people per day in order to achieve ‘full pandemic resilience’ by August

Medical laboratory scientists and clinical laboratory leaders know that the US’ inability to provide widespread diagnostic testing to detect SARS-CoV-2—the novel coronavirus that causes the COVID-19 illness—in the early stages of the outbreak was a major public health failure. Now a Harvard University report argues the US will need to deliver five million tests per day by early June—more than the total number of people tested nationwide to date—to safely begin reopening the economy.

“We need to deliver five million tests per day by early June to deliver a safe social reopening,” the report’s authors state. “This number will need to increase over time (ideally by late July) to 20 million a day to fully remobilize the economy. We acknowledge that even this number may not be high enough to protect public health. In that considerably less likely eventuality, we will need to scale-up testing much further. By the time we know if we need to do that, we should be in a better position to know how to do it. In any situation, achieving these numbers depends on testing innovation.”

The report is the work of a diverse group of experts in economics, public health, technology, and ethics, from major universities and big technology companies (Apple, Microsoft) with support from The Rockefeller Foundation.

“This is the first plan to show operationally how we can scale up COVID-19 testing sufficiently to safely reopen the economy—while safeguarding fundamental American democratic principles of protecting civil rights and liberties,” Danielle Allen, PhD (above), Director of Harvard University’s Edmond J. Safra Center for Ethics, said in a statement that noted it was “in response to the US Department of Health and Human Service’s Report to Congress on its COVID-19 strategic testing plan.” (Photo copyright: Harvard University.)

Under Harvard’s Roadmap plan, massive-scale testing would involve rapid development of:

Streamlined sample collection (for example) involving saliva samples (spit kits) rather than deep nasal swabs that have to be taken by healthcare workers;

Transportation logistics systems able to rapidly collect and distribute samples for testing;

Mega-testing labs, each able to perform in the range of one million tests per day, with automation, streamlined methods, and tightly managed supply chains;

Information systems to rapidly transmit test results; and

Technology necessary to certify testing status.

“The unique value of this approach is that it will prevent cycles of opening up and shutting down,” Anne-Marie Slaughter, CEO of New America, said in the statement. “It allows us to mobilize and re-open progressively the parts of the economy that have been shut down, protect our frontline workers, and contain the virus to levels where it can be effectively managed and treated until we can find a vaccine.”

Is Expanding Clinical Laboratory Testing Even Possible?

But is such a plan realistic? Perhaps not. When questioned by NBC News about the timeline for “broad-based coronavirus testing” that was suggested as part of the Trump Administration’s three-phase plan to reopen the states, former FDA Commissioner Scott Gottlieb, MD, said, “We’re not going to be there. We’re not going to be there in May, we’re not going to be there in June, hopefully, we’ll be there by September.”

In recent weeks, however, US testing capabilities have improved. Quest Diagnostics, which had come under fire for its testing backlog in California, announced it now has the capacity to perform 50,000 diagnostic COVID-19 tests per day or 350,000 tests per week with less than a two-day turnaround for results. “Our test capacity outpaces demand and we have not experienced a test backlog for about a week,” Quest said in a statement.

CDC ‘Modifies’ Its Guidelines for Declaring a Person ‘Recovered’ from COVID-19

Furthermore, the CDC modified its guidance on the medical and testing criteria that must be met for a person to be considered recovered from COVID-19, which initially required two negative test results before a patient could be declared “confirmed recovered” from the virus. The CDC added a non-testing strategy that allowed states to begin counting “discharged” patients who did not have easy access to additional testing as recovered from the virus.

Under the non-test-based strategy, a person may be considered recovered if:

At least three days (72 hours) have passed since recovery, defined as resolution of fever without the use of fever-reducing medications;

Improvement in respiratory symptoms (e.g., cough, shortness of breath); and,

At least seven days have passed since symptoms first appeared.

For now, however, the focus will likely remain on testing for those who are infected, rather than for finding those who have recovered. As of May 30, the COVID Tracking Project reported that only 16,495,443 million tests had been conducted in the US, with 1,759,693 of those test showing positive for COVID-19. That’s closing in on the 10% “test-positivity rate” recommended by the WHO for controlling a pandemic, but it’s not quite there.

As testing for COVID-19 grows exponentially, clinical laboratories should anticipate playing an increasingly important role in the nation’s response to the COVID-19 pandemic.

Medical laboratories are already using gene sequencing as part of a global effort to identify new variants of the coronavirus and their genetic ancestors

Thanks to advances in genetic sequencing technology that enable medical laboratories to sequence organisms faster, more accurately, and at lower cost than ever before, clinical pathology laboratories worldwide are using that capability to analyze the SARS-CoV-2 coronavirus and identify variants as they emerge in different parts of the world.

The US Centers for Disease Control and Prevention (CDC) now plans to harness the power of gene sequencing through a new consortium called SPHERES (SARS-CoV-2 Sequencing for Public Health Emergency Response, Epidemiology, and Surveillance) to “coordinate SARS-CoV-2 sequencing across the United States,” states a CDC news release. The consortium is led by the CDC’s Advanced Molecular Detection (AMD) program and “aims to generate information about the virus that will strengthen COVID-19 mitigation strategies.”

The consortium is comprised of 11 federal agencies, 20 academic institutions, state public health laboratories in 21 states, nine non-profit research organizations, and 14 lab and IVD companies, including:

Abbott Diagnostics

bioMérieux

Color Genomics

Ginkgo Bioworks

IDbyDNA

Illumina

In-Q-Tel

LabCorp

One Codex

Oxford Nanopore Technologies

Pacific Biosciences

Qiagen

Quest Diagnostics

Verily Life Sciences

‘Fundamentally Changing How Public Health Responds’

Gene sequencing and related technologies have “fundamentally changed how public health responds in terms of surveillance and outbreak response,” said Duncan MacCannell, PhD, Chief Science Officer for the CDC’s Office of Advanced Molecular Detection (OAMD), in an April 30 New York Times (NYT) article, which stated that the CDC SPHERES program “will help trace patterns of transmission, investigate outbreaks, and map how the virus is evolving, which can affect a cure.”

The CDC says that rapid DNA sequencing of SARS-CoV-2 will help monitor significant changes in the virus, support contact tracing efforts, provide information for developers of diagnostics and therapies, and “advance public health research in the areas of transmission dynamics, host response, and evolution of the virus.”

The sequencing laboratories in the consortium have agreed to “release their information into the public domain quickly and in a standard way,” the NYT reported, adding that the project includes standards for what types of information medical laboratories should submit, including, “where and when a sample was taken,” and other critical details.

Even in its early phase, the CDC’s SPHERES project has “made a tangible impact in the number of sequences we’re able to deposit and make publicly available on a daily basis,” said Pavitra Roychoudhury, PhD (above), Acting Instructor and Senior Fellow at the University of Washington, and Research Associate at Fred Hutchinson Cancer Research Center, in an e-mail to the NYT. “What we’re essentially doing is reading these small fragments of viral material and trying to jigsaw puzzle the genome together,” said Roychoudhury in an April 28 New York Times article which covered in detail how experts are tracking the coronavirus since it arrived in the US. (Photo copyright: LinkedIn.)

Sharing Data Between Sequencing Laboratories and Biotech Companies

The CDC announced the SPHERES initiative on April 30, although it launched in early April, the NYT reported.

According to the CDC, SPHERES’ objectives include:

To bring together a network of sequencing laboratories, bioinformatics capacity and subject matter expertise under the umbrella of a massive and coordinated public health sequencing effort.

To identify and prioritize capabilities and resource needs across the network and to align sources of federal, non-governmental, and private sector funding and support with areas of greatest impact and need.

To improve coordination of genomic sequencing between institutions and jurisdictions and to enable more resilience across the network.

To champion concepts of openness, standards-based analysis, and rapid data sharing throughout the United States and worldwide during the COVID-19 pandemic response.

To provide a common forum for US public, private, and academic institutions to share protocols, methods, bioinformatics tools, standards, and best practices.

To establish consistent data and metadata standards, including streamlined repository submission processes, sample prioritization criteria, and a framework for shared, privacy-compliant unique case identifiers.

To align with other national sequencing and bioinformatics networks, and to support global efforts to advance the use of standards and open data in public health.

Implications for Developing a Vaccine

As the virus continues to mutate and evolve, one question is whether a vaccine developed for one variant will work on others. However, several experts told The Washington Post that the SARS-CoV-2 coronavirus is relatively stable compared to viruses that cause seasonal flu (influenza).

“At this point, the mutation rate of the virus would suggest that the vaccine developed for SARS-CoV-2 would be a single vaccine, rather than a new vaccine every year like the flu vaccine,” Peter Thielen, a molecular biologist at the Johns Hopkins University Applied Physics Laboratory, told the Washington Post.

Nor, he said, is one variant likely to cause worse clinical outcomes than others. “So far, we don’t have any evidence linking a specific virus [strain] to any disease severity score. Right now, disease severity is much more likely to be driven by other factors.”

Fast improvements in gene sequencing technology have made it faster, more accurate, and cheaper to sequence. Thus, as the COVID-19 outbreak happened, there were many clinical laboratories around the world with the equipment, the staff, and the expertise to sequence the novel coronavirus and watch it mutate from generation to generation and from region to region around the globe. This capability has never been available in outbreaks prior to the current SARS-CoV-2 outbreak.

Limited availability of COVID-19 clinical lab tests is major topic at federal briefings and news stories, yet many of nation’s labs are laying off staff and at point of closing

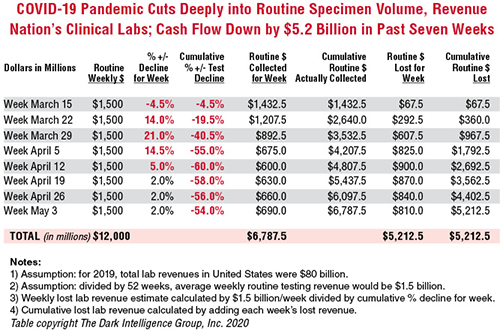

Cash flow at the nation’s clinical laboratories has crashed, with revenues down by more than $5 billion since early March. This is the biggest financial disaster for the nation’s clinical laboratory industry in its 100-year history and it couldn’t come at a worse time for the American public and the US healthcare system.

At the precise moment when the nation needs clinical laboratories to begin performing millions of tests for SARS-CoV-2, the coronavirus that causes the COVID-19 illness, those same labs are watching their cash flow collapse.

Data from multiple sources gathered by The Dark Report, sister publication of Dark Daily, confirm that—beginning in early March and continuing through last week—clinical laboratories in the United States saw incoming flows of routine specimens decline by between 50% and 60%. During this same time, lab revenue fell by similar amounts.

Clinical Lab Industry Currently Losing $800 to $900 Million Weekly

To give this decline context, the healthcare system spends about $80 billion annually on medical laboratory testing. Thus, labs across the US generated about $1.5 billion in revenue each week during 2019 and into 2020. By April 5, the decline in routine lab specimen volumes reached 55% to 60%. Since then, the clinical lab industry now loses between $800 million and $900 million each week. Total revenue loss from previous levels is already estimated to be $5.2 billion, and it is growing by an additional $800 million to $900 million every week that patients stay away from hospitals and physicians’ offices.

In the eight weeks since the COVID-19 pandemic caused patients to cease coming to hospitals and visiting their doctors, incoming routine specimens and revenue fell by 60%, causing cumulative lost routine revenue of $5.2 billion for the clinical laboratory industry in the United States. Each week that the existing shelter-in-place directives are effective, labs lose another $800 million to $900 million. The Dark Report based these estimates on data provided by multiple companies working with lab billing/claims, middleware analytical solutions, and customer relationship management (CRM) and electronic health record (EHR) products. (Chart copyright: The Dark Intelligence Group, Inc.)

The recent dire financial condition of labs small and large has gone unremarked by federal healthcare officials at the daily White House COVID-19 Task Force briefings. National news sources have yet to report on this development and its implications for successfully expanding the availability and numbers of COVID-19 tests in response to the pandemic.

The rapid and deep decline in specimens and revenue is not limited to clinical laboratories. Biopsy cases referred to anatomic pathology groups have declined by 50% to 60%. Some subspecialty pathology labs saw case referrals drop by 80% or more.

The nation’s two biggest clinical laboratory companies confirmed similar declines in their normal daily flow of routine specimens. Both companies recently reported first-quarter earnings (which included the month of March).

Quest Diagnostics, LabCorp Each Disclose Volume Declines of 50% to 60%

During its Q1 2020 earnings conference call, Chairman, President, and CEO of Quest Diagnostics (NYSE:DGX), Steve Rusckowski, stated, “In April, volume declines continue to intensify as we are seeing signs that volume declines are bottoming out at around 50% to 60%.”

The drop-off in routine lab test referrals was the similar at LabCorp (NYSE:LH). “In our diagnostics business, at the end of the quarter, we experienced reductions in demand for testing of 50% to 55% versus the company’s normal daily levels,” explained Glenn Eisenberg, Executive Vice President and CFO during LabCorp’s Q1 2020 earnings call. “This reduction in demand impacted testing volume broadly but was more heavily weighted towards routine procedures.”

Interviews with independent clinical lab owners and the administrative directors of hospital and health system labs further confirm this rapid and dramatic decline in the number of routine specimens arriving in their labs. Fewer specimens mean fewer claims, which means less revenue to laboratories.

Two Different Financial Futures for ‘Have’ Labs and ‘Have Not’ Labs

What happens next to the clinical laboratory industry in the United States—and to its ability to continue ramping up the availability of adequate numbers of COVID-19 tests in major cities, small towns, and rural areas—will be a story of “haves” and “have nots.”

The “haves” are clinical labs that have access to money. These are publicly-traded lab companies, academic medical center labs, and the sophisticated labs of health networks that operate multiple hospitals. In each case, these organizations have capital reserves and access to loans that will probably enable them to sustain COVID-19 lab testing services at the large volumes required to respond to the pandemic.

clinical labs operated by community hospitals and rural hospitals that were not financially robust before the onset of the pandemic; and,

specialty lab companies that perform a specific number of proprietary diagnostic tests (and for which demand has collapsed as patients stopped seeing their doctors).

Medicare Led Payers in the ‘Lab Test Price Race to the Bottom’

Prior to the onset of the SARS-CoV-2 pandemic, the finances of the “have-not” labs were already shaky, with many on the verge of filing bankruptcy, closing, or selling to a bigger lab company. Much blame for the deteriorating finances at a large proportion of community lab companies, community hospital labs, and rural hospital labs can be attributed to the deep, multi-year price cuts to the Medicare Part B clinical laboratory fee schedule as mandated by the Protecting Access to Medicare Act of 2014 (PAMA).

Medicare’s multi-year cuts to lab test prices were immediately copied by most state Medicaid programs. During this period, private payers followed Medicare’s lead and enacted their own deep cuts to the prices they paid labs for both routine tests and molecular/genetic tests.

That is why—when the pandemic intensified in early March—the 50% to 60% drop in specimens and revenue that hit these labs starved them of essential cash flow. When polled, the owners and directors of these labs acknowledge layoffs of the majority of their staff in all departments. They also reported substantial delays—both in submitted lab test claims and in getting payment for those claims—because claims-processing departments at the labs and private health insurers are understaffed due to shelter-in-place directives.

COVID-19 Test Revenue Helps Only Labs Performing Those Tests

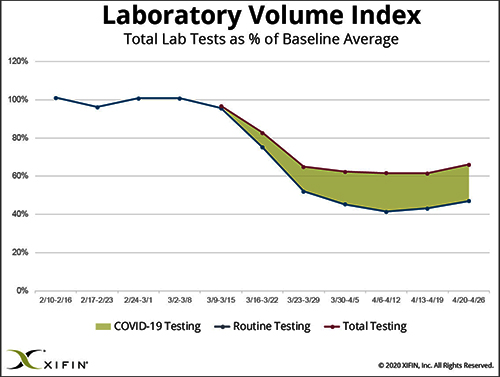

Revenue from COVID-19 testing is helping certain labs offset the revenue loss from fewer routine specimens. XIFIN, Inc., a San Diego company that provides revenue cycle management (RCM) services for clinical laboratories and pathology groups, analyzed the lab test claims for COVID-19 rapid molecular tests. It determined that labs performing these tests are generating enough revenue from these test claims to equal about 20% of their pre-pandemic revenue.

The chart above was prepared by XIFIN, Inc., of San Diego and is based on the changes XIFIN observed in the volume of routine clinical laboratory test claims generated by client labs on a weekly basis. In the first two months of 2020, routine lab test claims ran at expected levels until the first week of March. During the rest of March, routine lab test claims declined by 60%. During April, incoming routine lab test claims remained 55% to 60% below pre-pandemic levels. The shaded area shows the number of COVID-19 test claims coming into clinical labs. XIFIN says COVID-19 test claims make up about 20% of the decline in routine test specimens for those labs performing COVID-19 tests. The Dark Report estimates that the clinical laboratory industry has lost $800 million to $900 million in routine test revenue each week since March 23. Weekly revenue losses will continue at this rate until patients begin visiting their physicians and hospitals again perform elective services. (Chart copyright: XIFIN, Inc.)

Many CLIA-certified community laboratories and hospital labs have the diagnostic instruments and experience to perform rapid molecular tests for COVID-19. But when contacted, they tell us that their suppliers do not ship them even minimal quantities of the COVID-19 kits, the reagents, and the consumables. Thus, they cannot meet the needs of their client physicians. Instead, they watch as these physicians refer COVID-19 tests to the nation’s largest labs. The supply shortage prevents these smaller labs from doing larger numbers of COVID-19 test for the patients in the communities they serve. It also prevents them from earning the revenues from COVID-19 testing that currently helps the nation’s “have” labs offset the decline in revenue from routine testing.

Congress, national healthcare policymakers, and state governors need to immediately address this situation. Each week that passes during the COVID-19 pandemic and the shelter-in-place directives drains another $800 million to $900 million in revenue from routine lab testing that previously flowed into the nation’s clinical laboratories.

‘Have-not’ Clinical Labs in Small Towns Will Quietly Shrink and Disappear

Without timely intervention and financial support, the nation’s network of ‘have not’ labs, which have so capably served towns away from big metropolitan centers and rural areas, will quietly begin shrinking. One at a time, labs in small towns will close or sell. Local lab facilities will be shuttered and specimens from small-town patients will be transported to big labs hundreds or thousands of miles away.

It is also true that the financial disaster besetting the nation’s clinical laboratory industry will have comparable dramatic consequences for the in vitro diagnostics (IVD) manufacturers that sell them automation, analyzers, reagents, and other supplies. Since early March, IVD manufacturers watched as the pandemic caused orders for new instruments to collapse. During these same weeks, their clinical lab customers ceased ordering routine test kits at pre-pandemic levels. Dark Daily will cover the challenges confronting the IVD and other diagnostics industries in future e-briefings.

Announcing Free COVID-19 STAT Intelligence Briefings for Clinical Labs

With the COVID-19 pandemic creating chaos in nearly every aspect of healthcare, business, and society, clinical labs and their suppliers need timely intelligence and analysis about the innovations and successes achieved by their peers. This week, Dark Daily and The Dark Report are launching COVID-19 STAT Intelligence Briefings (Copy and paste this URL into your browser: https://www.covid19briefings.com). This comprehensive service is free and will cover four basic areas of needs for clinical laboratories as they ramp up COVID-19 testing:

Daily and weekly COVID-19 testing dashboards to guide every lab’s short-term planning;

Proven steps for labs to introduce and validate COVID-19 tests (both rapid molecular tests and serology tests);

Getting paid for COVID-19 testing to ensure every lab’s financial stability and clinical quality; and

Legal and regulatory updates for labs doing COVID19 tests to ensure full compliance.

Also, to help clinical laboratory leaders deal with the coming wave of COVID-19 serology tests, we are producing a free webinar led by James O. Westgard, PhD, FACB, and Sten Westgard, Director of Client Services and Technology, of Westgard QC, Inc.

Each week that the SARS-CoV-2 pandemic continues, and strict shelter-in-place directives are in place, the clinical laboratory industry loses another almost $900 million in revenue from lower volumes of routine testing. No industry can survive when its incoming revenue collapses by 50% to 60% for sustained periods of time.

Will Congress Recognize the Need for a Financial Rescue of ‘Have-not’ Labs?

Thus, it is incumbent on Congress, elected officials, and healthcare policymakers to recognize the financial consequences of the pandemic to the nation’s clinical laboratories. That is particularly true of the ‘have-not’ clinical labs. They do not have the same access to decisionmakers in government as billion-dollar lab companies.

And yet, these labs located in small communities and rural areas often are the only local labs that can do STAT testing in a couple of hours, and where clinical pathologists are personally familiar with local physicians and patients.

These “have-not” labs are vital healthcare resources. They should receive the help they need to get through this unprecedented crisis that is the COVID-19 pandemic.