Clinical laboratories should prepare to receive test orders from these mini-medical centers, based on consumer demand for quick, inexpensive, local healthcare

Is the era of clinical laboratory testing offered in retail stores soon to arrive? Dark Daily as long as 10 years ago predicted that walk-in clinics featuring a nurse or nurse practitioner who could diagnose and prescribe for a limited number of health conditions—which had a remedy that could be purchased at the pharmacy in the retail store—would be the door-openers to locating more sophisticated clinical services in retail settings.

Since then, we’ve covered many such openings—including free standing urgent care clinics opening in urban settings to service the consumer demands of busy patients—which have impacted clinical laboratories and anatomic pathology groups in predictable ways.

The premise of the collaboration was based around the belief that consumers would welcome the opportunity and benefits of receiving basic healthcare services in a facility located next to a pharmacy. The Walgreens/MedExpress agreement, however, also indicates that two of the largest healthcare organizations in the world believe consumers would also be interested in visiting physicians who provided more sophisticated medical services, including critical care, in retail settings.

To date, Walgreens has opened MedExpress clinics in 15 locations in six states, including: Minnesota, Nebraska, Nevada, Texas, Virginia, and West Virginia. More such clinics are expected to open this year as part of the collaboration.

“MedExpress is a resource for busy families and employers that need timely access to affordable, high-quality healthcare close to home and work,” Fred Hinz (above), VP of Operations at MedExpress told Drug Store News. “Being connected to Walgreens will enable our patients to receive quality care and purchase any other items they need, all in one trip.” It also will likely result in increased orders for clinical laboratory testing from retail locations. (Photo copyright: Grand Island Independent.)

Future Health System Delivers Critical Care from Retail Locations

Motivated by consumer demand for convenient, high-quality healthcare, the urgent care market in the United States continues to grow. This trend will eventually influence clinical laboratories and anatomic pathology groups seeking to service these providers. It will be a dynamic market as new participants and mergers compete for leverage in this profitable business.

“This is just part of developing an overall higher-performing local health system,” Forbes reported UnitedHealth CEO David Wichmann telling analysts during the company’s earning call last month. “It’d just be one component that may be nested inside a local care delivery market with ambulatory surgical capacities and house calls and things of that nature. This is the future health system that we see delivering considerable value to people.”

The speedy growth in the number of and profitability of urgent care centers is another confirmation that this healthcare trend has legs. And experts believe the growth will continue and accelerate.

A recent report by market research and consulting firm MarketsandMarkets (MnM) predicts the global urgent care market should reach $25.93 billion (US) by the year 2023. The current value of the industry is $20 billion. The growth rate for the industry is expected to be 5.3% with North America being the region accounting for the highest amount of that growth.

The MnM report attributes the rise in the urgent care market to many factors, including:

Growing investments in urgent care;

Strategic developments between urgent care providers and hospitals;

Access to affordable care;

Convenience of shorter wait times; and,

Increase in the geriatric population.

The report projects that the biggest hurdle facing the urgent care industry will be the lack of a skilled workforce.

Urgent Care a Growth Industry According to Experts

There are currently more than 7,500 urgent care facilities in the United States, according to an Urgent Care Association (UCA) white paper.

According to the UCA, the top six urgent care organizations in the US each have more than 100 locations. Those companies include:

A 2017 UCA benchmarking report states that only 3% of patients who are seen at an urgent care facility were diverted to an emergency room in 2016. The top diagnosis codes for visits during that year were:

A report by Becker’s Hospital Review states that urgent care visits account for 19% of all healthcare visits in the US.

Urgent Care Centers Badly Needed and Highly Profitable

Last year, strategy consulting firm Health Systems Advisors (HSA) commissioned a study regarding the current and future need for urgent care centers. According to Becker’s Hospital Review, the HSA study stated that:

“With the recent rise of urgent care development, there is an estimated 22% unmet need for urgent care in markets where urgent care sites could be financially viable;

“The unmet demand is so large that approximately 1,600 new urgent care sites can be supported generating nearly $3.5 billion in revenue; and,

“For health systems seeking to grow, the urgent care channel presents a unique opportunity to grow their revenue, influence patients’ downstream choices, and create a better experience for individuals desiring more convenience and better access.”

And data collected by FAIR Health indicates that, between 2007 and 2016, insurance claims for urgent care visits grew by a whopping 1,725%! Claims for emergency room visits increased by 229% during the same time period. FAIR Health is a non-profit organization that examines insurance claims for medical services for the purpose of bringing transparency to healthcare costs and insurance information.

Opportunities for Clinical Laboratories to Support Physicians

Clinical laboratories and pathology groups should pay attention to the burgeoning trend in urgent care, as those facilities order medical tests that will require processing, reading, and analyzing.

Exploring opportunities to serve urgent care centers offers clinical laboratories potential revenue streams and opportunities to serve the physicians practices and medical communities they support.

Primary care is shifting from traditional office visits to urgent care and walk-in clinics even as large hospital groups continue to buy up independent physician practices, altering where and from whom clinical laboratories receive referrals and test orders Medical test ordering and referrals from office-based physicians are the financial foundation of the clinical laboratory industry. Thus, recent trends reshaping how and where physicians practice medicine, and the ownership of their medical...

Since the first retail clinic opened in Minneapolis in 2001, there has been a steady increase in the number of such clinics, typically located in retail pharmacies and chain retailers

In Minnesota, UnitedHealth Group (NYSE:UNH) is preparing to substantially increase the number of urgent care clinics it operates in the state. These retail-style clinics will be operated by MedExpress, a company that UnitedHealth acquired in 2015.

UnitedHealth’s decision to expand the number of MedExpress retail clinics it operates, both in Minnesota and nationally, is a sign to clinical laboratory managers and pathologists that consumer demand for health services delivered by a retail clinic continues to increase. (more…)

Ongoing increases in the global number of prostate cancer cases expected to motivate test developers to deliver better screening tests to pathologists and clinical lab scientists

No less an authority than the peer-reviewed healthcare journal The Lancet is drawing attention to predictions of increasing prostate cancer cases across the globe, triggering calls for the development of cheaper, faster, and more accurate assays that pathologists and medical laboratories can use to screen for—and diagnose—prostate cancer.

Swift population growth and rising life expectancy will cause the prostate cancer death rate to nearly double in the next 20 years, according to a new study that has led scientists to call for immediate, critical improvements in clinical laboratory testing for cancer screening, Financial Times (FT) reported.

“Low- and middle-income countries need to prepare to prevent a sharp rise in fatalities while richer nations should pay more attention to young men at higher risk of the disease,” FT noted. The study, titled, “The Lancet Commission on Prostate Cancer: Planning for the Surge in Cases,” predicts cases will jump from 1.4 million in 2020 to 2.9 million by 2040.

“Prostate cancer is the most common cancer in men in 112 countries, and accounts for 15% of cancers. In this Commission, we report projections of prostate cancer cases in 2040 on the basis of data for demographic changes worldwide and rising life expectancy. … This surge in cases cannot be prevented by lifestyle changes or public health interventions alone, and governments need to prepare strategies to deal with it,” the study authors wrote.

“The findings in this Commission provide a pathway forward for healthcare providers and funders, public health bodies, research funders, governments, and the broader patient and clinical community,” the authors noted. In their Lancet paper, the researchers define clear areas for improvement.

Given the shortage worldwide of pathologists—especially highly-trained pathologists—the gap between the demand/need for expanded prostate cancer testing as screens (along with prostate biopsies) and the available supply of pathologists will encourage companies to develop screening and diagnostic tests that are accurate and automated, thus increasing the productivity of the available pathologists.

“As more and more men around the world live to middle and old age, there will be an inevitable rise in the number of prostate cancer cases. We know this surge in cases is coming, so we need to start planning and take action now,” said Nick James, PhD (above), Professor of Prostate and Bladder Cancer Research at The Institute of Cancer Research, in a press release. Pathologists and medical laboratories worldwide will want to monitor progress of The Lancet Commission’s recommendations. (Photo copyright: Institute of Cancer Research.)

“Evidence-based interventions, such as improved early detection and education programs, will help to save lives and prevent ill health from prostate cancer in the years to come. This is especially true for low- and middle-income countries (LMICs) which will bear the overwhelming brunt of future cases,” he said in a press release.

Communication is key. “Improved outreach programs are needed to better inform people of the key signs to look out for and what to do next,” James N’Dow, MD, Professor and Chair in Surgery and Director of the Academic Urology Unit at the University of Aberdeen in the UK, told the Financial Times. “Implementing these in tandem with investments in cost-effective early diagnostic systems will be key to preventing deaths,” he added.

Capitalizing on artificial intelligence (AI) analysis to help translate results was another area The Lancet Commission researchers focused on, Financial Times noted.

AI could “subdivide disease into potentially valuable additional subgroups to help with treatment selection. In environments with few or no pathologists, these changes could be transformational,” the study authors wrote.

High Income Countries (HICs) would benefit from AI by empowering patients. “Linking cloud-based records to artificial intelligence systems could allow access to context-sensitive, up-to-date advice for both patients and health professionals, and could be used to drive evidence-based change in all settings,” the study authors added. Such a trend could lead to specialist prostate cancer pathologists being referred cases from around the world as digital pathology systems become faster and less expensive.

Effective treatment strategies and bolstering areas of need is also key, the study notes. “Many LMICs have urgent need for expansion of radiotherapy and surgery services,” the study authors wrote. The researchers stress the need to immediately implement expansion programs to keep up with anticipated near-future demand.

Cancer drug therapy should follow suit.

“Research and the development of risk-stratified regulatory models need to be facilitated,” the study authors noted, citing a focus on drug repurposing and dose de-escalation. “Novel clinical trial designs, such as multi-arm platforms, should be supported and expanded,” they added.

Unique Needs of LMICs, HICs

The Lancet Commission researchers’ recommendations shift depending on the financial health of a specific area. HICs are experiencing a 30-year decline in the number of deaths resulting from prostate cancer, presumably from additional testing measures and public health campaigns that may be lacking in LMICs, Financial Times reported. And as population growth soars, low-to-middle income populations “will need to be prepared for the strain the expected surge in cases will put on health resources.”

For HICs, the study dissected the limitations of prostate-specific antigen (PSA) testing. The researchers pointed out that PSA’s inaccuracies in screening symptomless patients can pinpoint “cancers that may never cause symptoms and need no treatment,” Financial Times reported.

Missing high-risk cases was also a cause for concern. “Diagnostic pathways should be modified to facilitate early detection of prostate cancer while avoiding overdiagnosis and overtreatment of trivial disease,” the study notes.

Screenings for high-risk younger men, and continuing public campaigns about prostate cancer, should be a focus for HICs, the study authors noted. “These would include people who have a family history of the disease, are of African ancestry, or carry a genetic mutation known as BRCA2,” Financial Times reported.

While the undertaking may sound intimidating—there is already such a heavy impact worldwide from prostate cancer—the researchers are optimistic of their recommendations.

“Options to improve care are already available at moderate cost. We found that late diagnosis is widespread worldwide, but especially in LMICs, where it is the norm. Early diagnosis improves prognosis and outcomes, and reduces societal and individual costs, and we recommend changes to the diagnostic pathway that can be immediately implemented,” the study authors wrote.

What Comes Next

“More research is needed among various ethnic groups to expand understanding of prostate cancer beyond the findings from studies that were largely based on data from white men,” The Lancet Commission told the Financial Times.

Astute pathologists and medical laboratories will want to monitor efforts to develop assays that are inexpensive, more accurate, and produce faster answers. Demand for these tests will be substantial—both in developed and developing nations.

Nationwide, hospital losses are in the billions of dollars, which affects access to medical care including clinical laboratory testing

Hospitals and health systems across the United States continue to report substantial financial losses. At some institutions, this might severely restrict access to physicians and clinical laboratory testing for patients in those areas. The latest state to announce its hospitals were in trouble is Minnesota. The Minnesota Hospital Association (MHA) announced its hospitals are in “financial crisis” revealing that the state’s health systems experience hundreds of millions of dollars in operating losses annually.

The MHA stated that two out of three surveyed hospitals in Minnesota reported losing money in the cumulative amount of more than $400 million during the first half of 2023, KARE 11 reported. The MHA surveyed more than 70 health system members which represented facilities of all sizes and in all geographical regions of the state.

Rahul Koranne, MD, President and CEO of MHA told KARE 11 that part of the problem is that a larger proportion of patients rely on federal programs such as Medicare and Medicaid to pay hospital costs. Those programs provide lower reimbursement rates when compared to private insurers. In some facilities, almost 75% of patients are on one of these government programs.

“Those reimbursements, or payments, are fixed. So, we can’t raise prices. These two programs are paying significantly below the cost of providing care to our patients,” he noted. “So, if you have 70% of your patients covered by these governmental programs, we can’t raise prices, and they’re paying you below the cost of care—that’s what causes [the problem].”

He went on to state that workforce staffing represents a significant challenge for hospitals and urged the state legislature to address the needs of health professionals and facilities.

“We need to really resource it in this upcoming session and many sessions to come, so that we can have workers and staff we need,” Koranne said. “If we don’t have the money, and if we don’t have the workers, we will not be providing care and that would be sad.”

“This is a pretty grave state and, I would say, quite a crisis,” Rahul Koranne, MD (above), President and CEO of the Minnesota Hospital Association, told KARE 11. “Our not-for-profit hospitals and healthcare systems are hanging dangerously from this cliff and they’re getting tired.” Access to medical laboratory testing can be greatly affected by hospital financial losses. (Photo copyright: Twin Cities Business.)

Other US Healthcare Systems in Crisis as Well

Minnesota is not the only state with healthcare systems in financial crisis. Last year, the Washington State Hospital Association (WSHA) announced that hospitals in that state reported cumulative losses of $2 billion for 2022. Cassie Sauer, President and CEO of WSHA told the media that the massive deficits are “clear and incredibly concerning” to the state’s healthcare leaders.

In “Hospitals, Pharmacies Struggle to Be Profitable,” we reported that the WSHA survey determined that the state’s hospitals suffered collective operating losses of $750 million during the first six months of 2023.

“The financial losses that our hospitals are experiencing continue to be enormous,” Sauer told The Seattle Times. “Revenues simply are not keeping up with rapidly escalating costs. It’s most concerning as these large losses are putting patient care at risk in many communities across the state.”

The WSHA findings were based on a survey of 81 acute-care hospitals that represented about 98% of the state’s hospital beds. Of those facilities, 69 reported losing money mostly due to rising costs for supplies, labor, and other expenses as well as the need for longer hospital stays due to more complicated care and a larger percentage of patients on government programs, which offer lower reimbursement rates for care.

“When hospitals are not financially viable and over time sustain heavy losses, you must either increase revenue or reduce healthcare services,” Chelene Whiteaker, Senior Vice President, Government Affairs at WSHA, told The Seattle Times. “Reducing healthcare services is an option nobody wants on the table. So, that leaves increasing revenues.”

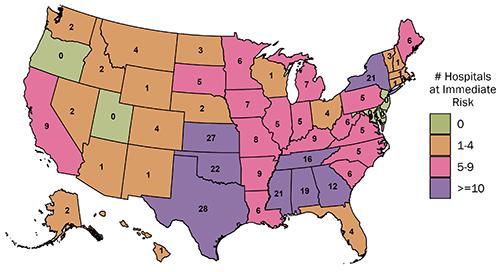

The graphic above from the Center for Healthcare Quality and Payment Reform (CHQPR) shows the number and location of rural hospitals in America that are at “immediate” risk of closure. The number of hospitals simply “at risk” of closure is substantially higher. Patients who depend on these hospitals would lose access to critical healthcare services including clinical laboratory testing. (Graphic copyright: Center for Healthcare Quality and Payment Reform.)

Becker’s Hospital Review reported last year that many hospitals across the country reported substantial losses in 2022. Three of the hospital systems in that article reported losses in the billions. They were:

In another article, Becker’s reported that 72 hospitals across the US closed departments or ended services in 2023. These cuts included the shuttering of health and urgent care clinics, the closure of outpatient cancer and pulmonary clinics, the reduction of certain surgical services and behavioral health services, and the ending of home healthcare services.

Some states are taking measures to prevent further hospital closures. But is it too late? In “California Doles Out $300 Million in No-Interest Loans to Save its Financially Struggling Hospitals,” The Dark Report’s sister publication Dark Daily covered how that state had launched an interest-free loan program to ensure local communities have access to community hospitals, their physicians, and clinical laboratories. No report on how many hospitals have been temporarily saved from closing thanks to this program.

If US hospitals continue to lose money at this rate, access to critical care—including clinical laboratory and anatomic pathology services—could be further restricted and facilities closed. These actions may also result in increased staff layoffs and have an even greater effect on patient care in Minnesota, Washington State, and throughout the US.