Legal, regulatory, and payer experts outline steps that help medical laboratories better navigate federal and state regulatory guidelines, eliminate coding and billing missteps, and maximize reimbursements

Even as daily COVID-19 test numbers continue to decrease, many clinical laboratories have substantial numbers of COVID-19 test claims that remain unpaid. Despite federal and state law requiring that labs be paid for these tests, commercial health plans are using many strategies to avoid paying labs for COVID-19 test claims.

That means a large portion of the nation’s labs are owed tens of thousands, hundreds of thousands, even millions of dollars for unpaid SARS-CoV-2 test claims they submitted since the onset of the pandemic last year.

What Clinical Labs Can Do to Be Paid for Their COVID-19 Test Claims

These four subject-matter experts provided insider tips and insights on steps clinical laboratories can take to get paid for COVID-19 test claims. This advice can help labs, maximize collected dollars, reduce the chance of post-payment audits, and navigate emerging payer trends.

During the webinar, Caitlin Forsyth, an Associate Attorney at Davis Wright Tremaine LLP in Seattle who specializes in healthcare regulatory compliance, said the new guidance “impressed upon commercial health plans the requirement to cover COVID testing in a lot of different circumstances.” The guidance included information on how providers can be reimbursed for providing COVID-19 care to uninsured people.

However, labs should be aware of what may come after they receive payment.

“We applaud you if you’ve had success thus far in securing reimbursement,” Forsyth continued. “However, clinical laboratories are not necessarily home free if Medicare, Medicaid, or a health plan has paid all or most of the lab claims for COVID-19 tests. This is because the payer may at some point down the line require the laboratory to submit to a post-payment audit. As part of the audit, the government payer or health plan is likely to require a laboratory to provide supporting documentation underscoring the medical necessity of each test performed on each patient at issue.”

What Constitutes ‘Medical Necessity’ for a SARS-CoV-2 Test?

There are many tripwires that can derail COVID-19 test claims. Medical necessity standards related to testing is one example that has been a major area of concern for clinical laboratories.

Kathryn Edgerton, Esq., Counsel at Davis Wright Tremaine LLP in Los Angeles, notes that the guidance providers have received has been “somewhat inconsistent and has created confusion as to what test is covered.” This lack of clarity in Medicare’s guidance has caused many denials of payment.

This Special Report from Dark Daily is the companion to the recent Dark Daily webinar on “Getting Paid for COVID-19 Test Claims: Prepare for Audits, Maximize Reimbursement and Navigate Payer Trends.” Clinical laboratory professionals can download the report by clicking here. (Photo copyright: Dark Daily.)

The webinar panelists provided the following three tips for optimizing billing claims for COVID-19 tests (additional recommendations on decreasing the number of COVID-19 test claim denials, increasing payments, and avoiding post-payment audits are available in the webinar’s on-demand replay and its companion special report):

When seeking reimbursement for COVID-19 testing from non-traditional sources, such as employers, schools, or local governments, ensure valid orders support each test claim. “Even if the employer, school, or local government has agreed to pay for the tests, a medical laboratory still must comply with state laws in regard to persons authorized to order the tests, as well as comply with CLIA requirements for a valid order,” Forsyth said.

Serial testing is on the rise in workplaces to increase the chances of detecting asymptomatic infection. However, Forsyth says, laboratories should “push for direct reimbursement from the workplace” because coverage from Medicare, Medicaid, and health plans is uncertain. “We also expect health plans to start cracking down on tests performed as part of an employment or surveillance program, taking the position that even if there are physician orders supporting each test performed as part of the program, health plans are not required to cover tests,” she added.

COVID-19-only testing providers and independent laboratories should expect health plans to begin narrowing their provider networks. To avoid being pushed out, Steve Stonecypher, Managing Partner at Shipwright Healthcare Group, says laboratories should “think about what you do, how you do it, and how you can be a benefit [to the health plan]. Make the payers think of you not as a nice-to-have in their network, but as a need-to-have in their network.”

COVID-19 Testing Labs Advised to ‘Have All Your Ducks in a Row’

Stonecypher urges clinical laboratories to be vigilant in record keeping, noting that the US Department of Health and Human Services Office of Inspector General (OIG) indicated earlier this year that it will conduct audits that focus on aberrant billing for COVID-19 testing during the pandemic.

“There are flags out there already that the OIG is potentially going to look to do claim audits,” he said. “You can pretty much guarantee that the payers are going to follow. So, have all your ducks in a row. We’re talking about all the individual patient assessments, all that necessary documentation … make sure all of that is in order because payers are going to look at this as an opportunity to come back and recoup money.”

Billing and finance executives, clinical laboratory leadership, compliance officers, and billing and coding administrators are especially encouraged to listen to this webinar about increasing the number of COVID-19 test claims for which the lab is reimbursed. This webinar is available to stream on-demand.

This can be one of the best low-cost, high return investments your lab team can make, particularly if it helps the lab’s coding/billing/collections team interact with health insurance plans to settle SARS-CoV-2 test claims that then bring in tens of thousands or hundreds of thousands of dollars from outstanding claims that have yet to be paid.

Oddly, as upcoding severity levels have risen, reported higher-severity inpatient hospital stays have dropped, OIG reported

Medicare upcoding fraud is a growing problem for the federal Centers for Medicare and Medicaid Services (CMS). Now, a report from the US Department of Health and Human Services (HHS) Office of Inspector General (OIG) suggests that the practice is increasingly occurring for high-severity inpatient hospital stays that account for the most expensive part of US healthcare.

“The [COVID-19] pandemic has placed unprecedented stress on the country’s healthcare system, making it more important than ever to ensure that Medicare dollars are spent appropriately,” the OIG report states.

The OIG website notes, “Medicare pays for many physician services using Evaluation and Management (commonly referred to as “E/M”) codes. New patient visits generally require more time than follow-up visits for established patients, and therefore E/M codes for new patients command higher reimbursement rates than E/M codes for established patients.”

The OIG describes one type of upcoding as “… an instance when [providers] provide a follow-up office visit or follow-up inpatient consultation, but bill using a higher-level E/M code as if [they] had provided a comprehensive new patient office visit or an initial inpatient consultation.

“Another example of upcoding related to E/M codes is misuse of Modifier 25,” the OIG continued. “Modifier 25 allows additional payment for a separate E/M service rendered on the same day as a procedure. Upcoding occurs if a provider uses Modifier 25 to claim payment for an E/M service when the patient care rendered was not significant, was not separately identifiable, and was not above and beyond the care usually associated with the procedure.”

How OIG Conducted the Study of Hospital Coding Practices

To perform its research, the OIG analyzed Medicare Part A claims for hospital stays for the six-year period from fiscal year (FY) 2014 through FY 2019. The OIG identified trends in billing and payments for inpatient hospital stays at the highest severity levels, as determined by the Medicare Severity Diagnosis Related Group (MS-DRG).

The OIG investigation revealed that the number of hospital stays billed at the highest severity level increased almost 20% between 2014 and 2019, while the number of stays billed at other severity levels decreased. These expenditures accounted for nearly half of all Medicare spending on inpatient hospital stays, the OIG reported.

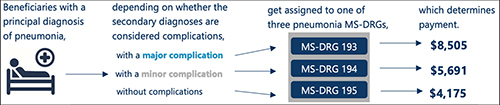

According to the OIG report, “Medicare pays hospitals more for beneficiaries in MS-DRGs with higher severity levels because they are typically more costly to treat.” The graphic above taken from the OIG report illustrates “how the presence of complications can affect Medicare payment for three beneficiaries with the same principal diagnosis.” (Graphic copyright: Federal Office of Inspector General Department of Health and Human Services.)

As Severity Levels Went Up, Inpatient Length of Stays Went Down

Interestingly, the average length of inpatient stays at the highest severity level decreased, and the average length of hospital stays overall remained largely the same, decreasing by just 0.1 days. In addition, the total number of inpatient hospital stays decreased by 5%.

The OIG report noted that “the increase in the number of stays billed at the highest severity level implies that beneficiaries were sicker overall. However, the decrease in the average length of stays at the highest severity level potentially undermines that idea because it is not consistent with sicker beneficiaries. Length of stay generally has a positive relationship to severity of stay; sicker beneficiaries stay in the hospital longer.”

The OIG confirmed that in FY 2019, Medicare spent $109.8 billion for 8.7 million hospital stays. Approximately 3.5 million (or 40%) of those stays were billed at the highest severity level, as determined by the MS-DRG. In addition, nearly half of the $109.8 billion spent, or $54.6 billion, was for stays billed at the highest severity level and Medicare paid an average of $15,500 per stay at that level.

The OIG report states that “stays at the highest severity level are vulnerable to inappropriate billing practices, such as upcoding—the practice of billing at a level that is higher than warranted. Specifically, nearly a third of these stays lasted a particularly short amount of time and over half of the stays billed at the highest severity level had only one diagnosis qualifying them for payment at that level. Further, hospitals varied significantly in their billing of these stays, with some billing much differently than most.”

The OIG study also found that over half of the inpatient stays billed at the highest severity level achieved that level due to only one diagnosis. According to the OIG, the severity of an inpatient stay depends on a patient’s secondary diagnosis and it only takes one secondary diagnosis to propel a patient into the highest severity level. The OIG determined that if the diagnosis was inaccurate or inappropriate, higher payments would not be warranted.

OIG Recommends CMS Conduct Targeted Reviews

The report found that the most frequently billed MS-DRG in FY 2019 was septicemia or severe sepsis and that hospitals billed for 581,000 of these stays, for which Medicare paid $7.4 billion. In addition, kidney and urinary tract infections, pneumonia, and renal failure were among the most common conditions to have a complication that led to a high severity classification.

In its report, the OIG recommended more oversight from CMS to ensure that Medicare dollars are spent appropriately. The OIG also suggests that CMS conduct targeted reviews of MS-DRGs and hospital stays that are vulnerable to upcoding, as well as the hospitals that frequently bill them.

Clinical Laboratories Are Forewarned

Medicare audits continue to be more detailed and rigorous and all healthcare providers—including clinical laboratories and anatomic pathology groups—should be prepared to present all necessary documentation to support claims if and when they are audited.

Improvements in software, machine learning, and artificial intelligence (AI) give Medicare officials and the OIG powerful tools to spot questionable provider billing. This includes medical laboratories whose billing patterns could arouse suspicions and trigger audits.

Upcoding is a long-standing problem for the Medicare program. What is changing is that federal officials now have better tools and resources to use in identifying patterns of upcoding that fall outside accepted parameters.

Physician use of genetic tests continues to grow at robust rates, even during the pandemic, but uncertainty about managed care reimbursement hangs over the market

It may surprise many pathologists and clinical laboratory managers to learn that the market for genetic testing is robust and growing swiftly, even in the midst of the COVID-19 pandemic. At the same time, the explosion in both the number of unique genetic tests available to physicians, and the willingness of doctors to order genetic tests for their patients, are creating major challenges for both government and private payers.

Moreover, how payers are attempting to gain control over this boom in genetic testing is creating serious problems for genetic testing companies seeking reimbursement for their test claims. This is because health insurers are taking aggressive steps to control their spending on genetic tests. Some of those steps include:

Prior-authorization requirements for an ever-larger number of genetic tests.

Reducing the prices paid for high-cost genetic tests.

Tough audits that use sampling and extrapolation and produce sizeable recoupment demands.

Unexpected Developments in Genetic Test Marketplace

These are reasons why clinical laboratories need to fully understand the state of the genetic testing market. Physicians are receptive to ordering genetic tests that will improve the care they provide their patients. But health insurers want better control over the unplanned and substantial increases in the total amount of money they pay out for the surging number of genetic test claims.

Collectively, these developments confront genetic testing companies with a mix of good news and bad news. The good news is that more physicians are using genetic tests in their daily medical practice. The bad news is that many payers are erecting ever-more restrictive hurdles that labs must overcome when submitting genetic test claims and seeking adequate payment.

Strategic Insights into What’s Changing with Genetic Testing

This webinar will be one of the most important strategic assessments of genetic testing presented to the clinical laboratory and diagnostics industries since the COVID-19 pandemic began last March. Your presenters are recognized thought-leaders in the genetic testing and laboratory medicine industries. Speaking in order are:

Bruce Quinn, MD, PhD, Principal, Bruce Quinn Associates LLC, Los Angeles: An expert in how Medicare and private payers establish coverage guidelines and prices for new genetic tests, Dr. Quinn will explain the key differences in how private payers are managing genetic test utilization and payment, compare to the federal Medicare program.

Heather Agostinelli, Asst. Vice President, Strategic Revenue Operations, XIFIN Inc., San Diego: Heather will provide a detailed perspective on the daily actions by payers as they process claims and issue payment for genetic tests. She will also present recommendations for how labs can optimize the number of clean genetic test claims, thus helping shorten payment times in ways that improve cash flow.

Rob Metcalf, CEO, Concert Genetics, Nashville, Tenn.: He will discuss the scope and scale of the explosion in the number of genetic test claims by sharing data, charts, and analyses usually only available to clients.

Your Chair and Moderator will be Robert L. Michel, Editor-in-Chief of The Dark Report.

The purpose of the upcoming webinar includes helping attendees with the following and more:

Learn why payers must now deal with more than 1,000 new genetic testing products launching every month and how that complicates claims processing.

Understand how the variation in CPT coding by different genetic testing labs complicates claims processing by payers.

Learn why “benefit investigation” is already a huge factor as consumers seek the lab with the cheapest genetic test price before they agree to be tested.

Master the art of working with prior authorization programs and know why having documents prior to authorization still does not necessarily mean the payer will reimburse for a genetic test claim.

Understand Medicare’s policy changes at the national level for genetic tests.

Know the core elements of the Medicare MolDx program that gov-erns genetic test claims across 28 states.

Valuable Information for Financial Analysis, Managed Care Executives

In addition to bringing clinical pathologists and directors/managers of clinical laboratories up to date on the genetic testing marketplace, this webinar will provide valuable insights into financial analysts’ tracking of genetic testing companies, managed care executives’ handling of genetic testing claims, genetic counselors, and others involved in managing clinical service lines that utilize genetic tests in patient care.

Called the Geographic Direct Contracting Model (GEO), CMS’ new “voluntary payment model” aims at giving providers of Medicare Part A and Part B services “a direct incentive to improve care across entire geographic regions,” according to a CMS press release.

“The Geographic Direct Contracting Model is part of the Innovation Center’s suite of Direct Contracting models and is one of the Center’s largest bets to date on value-based care,” Brad Smith, Deputy Administrator and Director of the Center for Medicare and Medicaid Innovation (CMMI), told RevCycleIntelligence. Smith is also the former CEO and co-founder of Aspire Health.

According to a CMS Fact Sheet, the GEO model “will test whether a geographic-based approach to value-based care can improve quality of care and reduce costs for Medicare beneficiaries across an entire geographic region.”

“This model allows participating entities to build integrated relationships with healthcare providers and invest in population health in a region to better coordinate care, improve quality, and lower the cost of care for Medicare beneficiaries in a community, said CMS Administrator Seema Verma in the CMS press release. Clinical laboratories may find opportunities as well, to collaborate with physicians in the clinical decision-making process. (Photo copyright: Business Insider.)

“Leveraging best practices and lessons learned from prior Innovation Center models, Geo will enable Direct Contracting Entities (DCEs) to build integrated relationships with healthcare providers and community organizations in a region to better coordinate care and address the clinical and social needs of Medicare beneficiaries,” the CMS Fact Sheet states.

“If we’re successful, we’ll move value-based care from something that might be 10 or 20% of somebody’s revenue to something that’s 80 or hopefully 100% of somebody’s revenue (in five to 10 years),” Smith told MedPage Today.

Healthcare providers and health plans that participate in the Geographic Direct Contracting model must be covered entities under the Health Insurance and Portability Accountability Act (HIPAA) and submit applications by April 2, 2021, the CMS fact sheet states.

The first performance period starts Jan. 1, 2022, and participation is voluntary. Direct contracting entities take “100% shared savings and shared losses for Medicare Part A and B services for aligned Medicare fee for service beneficiaries in a defined region,” the CMS fact sheet explained.

CMS is considering implementing the GEO model in Atlanta, Dallas, Denver, Detroit, Houston, Los Angeles, Miami, Minneapolis, Orlando, Phoenix, Philadelphia, Pittsburgh, Riverside, San Diego, and Tampa.

“By initially testing the model in a small number of geographies, we will be able to thoughtfully learn how these flexibilities are able to impact quality and costs,” Smith told RevCycleIntelligence.

How Will Value-Based Care Programs Affect Clinical Laboratories?

Value-based payment arrangements require doctors to accept changes to how they are reimbursed for their services. In kind, doctors are examining how clinical laboratories can take on an enhanced role in clinical decision making.

“Physicians and hospitals in a value-based environment need a different level of service and professional consultation from the lab and pathology group because they are being incented to detect disease earlier and be active in managing patients with chronic conditions to keep them healthy and out of the hospital,” said Robert Michel, Publisher and Editor-in-Chief of Dark Daily and its sister publication The Dark Report.

Michel explained that value-based care providers are calling on labs to go beyond reporting accurate test results within allotted turnaround times. “They want collaboration in identifying at-risk patients and in finding and closing gaps in care by using laboratory test results.”

Medical laboratory leaders may want to reach out to healthcare providers participating in value-based care models to explore areas of interest relating to patient population, chronic conditions, and severity of illness.

Clinical laboratories that offer testing and reporting and additionally collaborate with healthcare providers and health plans in ways that contribute to improved patient outcomes and lowered costs, may be in a position to earn any financial rewards from these and other new value-based arrangements.

CEOs of NorDx Laboratories, Sonora Quest Laboratories, and HealthPartners/Park Nicollet Laboratories expect demand for SARS-CoV-2 tests to only increase in coming months

The short answer is that large volumes of COVID-19 testing will be needed for the remaining weeks of 2020 and substantial COVID-19 testing will occur throughout 2021 and even into 2022. This has major implications for all clinical laboratories in the United States as they plan budgets for 2021 and attempt to manage their supply chain in coming weeks. The additional challenge in coming months is the surge in respiratory virus testing that is typical of an average influenza season.

Stan Schofield (above center), President of NorDx, a regional laboratory corporation that supports an integrated delivery system at MaineHealth in Portland, Maine.

Rick L. Panning (above right), MBA, MLS(ASCP)CM, retired as of Oct. 2 from the position of Senior Administrative Director of Laboratory Services for HealthPartners and Park Nicollet in Minneapolis-St. Paul, Minnesota.

Each panelist was asked how his parent health system and clinical laboratory was preparing to respond to the COVID-19 pandemic through the end of 2020 and into 2021.

First to answer was Panning, whose laboratory serves the Minneapolis-Saint Paul market.

A distinguishing feature of healthcare in the Twin Cities is that it is at the forefront of operational and clinical integration. Competition among health networks is intense and consumer-focused services are essential if a hospital or physician office is to retain its patients and expand market share.

Panning first explained how the pandemic is intensifying in Minnesota. “Our state has been on a two-week path of rising COVID-19 case numbers,” he said. “That rise is mirrored by increased hospitalizations for COVID-19 and ICU bed utilization is going up dramatically. The number of hospitalized COVID-19 patients has doubled during this time and Minnesota is surrounded by states that are even in worse shape than us.”

These trends are matched by the outpatient/outreach experience. “We are also seeing more patients use virtual visits to our clinics, compared to recent months,” noted Panning. “About 35% of clinical visits are virtual because people do not want to physically go into a clinic or doctor’s office.

“Given these recent developments, we’ve had to expand our network of specimen collection sites because of social distancing requirements,” explained Panning. “Each patient collection requires more space, along with more time to clean and sterilize that space before it can be used for the next patient. Our lab and our parent health system are focused on what we call crisis standards of care.

“For all these reasons, our planning points to an ongoing demand for COVID-19 testing,” he added. “Influenza season is arriving, and the pandemic is accelerating. Given that evidence, and the guidance from state and federal officials, we expect our clinical laboratory will be providing significant numbers of COVID-19 tests for the balance of this year and probably far into 2021.”

COVID-19 Vaccine Could Increase Antibody and Rapid Molecular Testing

Arizona is seeing comparable increases in new daily COVID-19 cases. “There’s been a strong uptick that coincides with the governor’s decision to loosen restrictions that allowed bars and exercise clubs to open,” stated Dexter. “We’ve gone from a 3.8% positivity rate up to 7% as of last night. By the end of this week, we could be a 10% positivity rate.”

Looking at the balance of 2020 and into 2021, Dexter said, “Our lab is in the midst of budget planning. We are budgeting to support an increase in COVID-19 PCR testing in both November and December. Arizona state officials believe that COVID-19 cases will peak at the end of January and we’ll start seeing the downside in February of 2021.”

The possible availability of a SARS-CoV-2 vaccine is another factor in planning at Dexter’s clinical laboratory. “If such a vaccine becomes available, we think there will be a significant increase in antibody testing, probably starting in second quarter and continuing for the balance of 2021. There will also be a need for rapid COVID-19 molecular tests. Today, such tests are simply unavailable. Because of supply chain difficulties, we predict that they won’t be available in sufficient quantities until probably late 2021.”

COVID-19 Testing Supply Shortages Predicted as Demand Increases

At NorDx Laboratories in Portland, Maine, the expectation is that the COVID-19 pandemic will continue even into 2022. “Our team believes that people will be wearing masks for 18 more months and that COVID-19 testing with influenza is going to be the big demand this winter,” observed Schofield. “The demand for both COVID-19 and influenza testing will press all of us up against the wall because there are not enough reagents, plastics, and plates to handle the demand that we see building even now.

“Our hospitals are already preparing for a second surge of COVID-19 cases,” he said.

COVID-19 patients will be concentrated in only three or four hospitals. The other hospitals will handle routine work. Administration does not want to have COVID-19 patients spread out over 12 or 14 hospitals, as happened last March and April.

“Administration of the health system and our clinical laboratory think that the COVID-19 test volume and demand for these tests will be tough on our lab for another 12 months. This will be particularly true for COVID-19 molecular tests.”

As described above, the CEOs of these three major clinical laboratories believe that the demand for COVID-19 testing will continue well into 2021, and possibly also into 2022. A recording of the full session was captured by the virtual Executive War College and, as a public service to the medical laboratory and pathology profession, access to this recording will be provided to any lab professional who contacts info@darkreport.com and provides their email address, name, title, and organization.

Robert L. Michel, Panelist—Publisher, Editor-in-Chief, The Dark Report and Dark Daily, Spicewood, Texas.

Given the importance of sound strategic planning for all clinical laboratories and pathology groups during their fall budget process, the virtual Executive War College is opening this session to all professionals in laboratory medicine, in vitro diagnostics, and lab informatics.

Financial losses for hospitals and health systems due to cancelled procedures and coronavirus expenses will lead to changes in healthcare delivery, operations, and clinical laboratory test ordering

COVID-19 is reshaping how people work, shop, and go to school. Is healthcare the next target of the coronavirus-induced transformation? According to two experts, the COVID-19 pandemic is pushing hospitals and health systems toward a “fundamental and likely sustained transformation,” which means clinical laboratories must be prepared to adapt to new provider needs and customer demands.

Burik and Fisher called attention to the staggering $50 billion-per-month loss for hospitals and health systems that was first revealed in an American Hospital Association (AHA) report published in May. The AHA report estimated a $200 billion loss from March 1, 2020, to June 30, 2020, due to increased COVID-19 expenses and cancelled elective and non-elective surgeries.

Adding to the financial carnage is the expectation that patient volumes will be slow to return. In “Hospitals Forecast Declining Revenues and Elective Procedure Volumes, Telehealth Adoption Struggles Due to COVID-19,” Burik said, “Healthcare has largely been insulated from previous economic disruptions, with capital spending more acutely affected than operations. But this time may be different since the COVID-19 crisis started with a one-time significant impact on operations that is not fully covered by federal funding.

“Providers face a long-term decrease in commercial payment, coupled with a need to boost caregiver and consumer-facing digital engagement, all during the highest unemployment rate the US has seen since the Great Depression,” he continued. “For organizations in certain locations, it may seem like business as usual. For many others, these issues and greater competition will demand more significant, material change.”

A Guidehouse analysis of a Healthcare Financial Management Association (HFMA) survey, suggests one-in-three provider executives expect to end 2020 with revenues at 15% below pre-pandemic levels, while one-in-five of them anticipate a 30% or greater drop in revenues. Government aid, Guidehouse noted, is likely to cover COVID-19-related costs for only 11% of survey respondents.

“The figures illustrate how the virus has hurled American medicine into unparalleled volatility. No one knows how long patients will continue to avoid getting elective care or how state restrictions and climbing unemployment will affect their decision making once they have the option,” Burik and Fisher wrote. “All of which leaves one thing for certain: Healthcare’s delivery, operations, and competitive dynamics are poised to undergo a fundamental and likely sustained transformation.”

As a result, the two experts predict these pandemic-related changes to emerge:

Payer-Provider Complexity on the Rise; Patients Will Struggle. As the pandemic has shown, elective services are key revenues for hospitals and health systems. But the pandemic also will leave insured patients struggling with high deductibles, while the number of newly uninsured will grow. Furthermore, upholding of the hospital price transparency ruling will add an unwelcomed spotlight on healthcare pricing and provider margins.

Best-in-Class Technology Will Be a Necessity, Not a Luxury. COVID-19 has been a boon for telehealth and digital health usage, creating what is likely to be a permanent expansion of virtual healthcare delivery. But only one-third of executives surveyed say their organizations currently have the infrastructure to support such a shift, which means investments in speech recognition software, patient information pop-up screens, and other infrastructure to smooth workflows will be needed.

“Through all the uncertainty COVID-19 has presented, one thing hospitals and health systems can be certain of is their business models will not return to what they were pre-pandemic,” Guidehouse Partner Chuck Peck, MD (above), a former health system CEO, said in a statement. “A comprehensive consumer-facing digital strategy built around telehealth will be a requirement for providers. Moreover, shifting hardware and physical assets to the cloud, and use of robotic process automation, has proven to be successful in improving back-office operations in other industries. Providers will need to follow suit.” Clinical laboratories and anatomic pathology groups should track these developments and respond appropriately to meet the changing needs of the hospitals and physicians they serve with diagnostic testing services. (Photo copyright: Athens Banner-Herald.)

The Tech Giants Are Coming. Both major retailers and technology stalwarts, such as Amazon, Walmart, and Walgreens, are entering the healthcare space. In January, Dark Daily reported on Amazon’s roll out of Amazon Care, a 24/7 virtual clinic, for its Seattle-based employees. Amazon (NASDAQ:AMZN) is adding to a healthcare portfolio that includes online pharmacy PillPack and joint-venture Haven Healthcare. Meanwhile, Walmart is offering $25 teeth cleaning and $30 checkups at its new Health Centers. Dark Daily covered this in an e-briefing in May, which also covered a new partnership between Walgreens and VillageMD to open up to 700 primary care clinics in 30 US cities in the next five years.

Work Location Changes Mean Construction Cost Reductions. According to Guidehouse’s analysis of the HFMA COVID-19 survey, one-in-five executives expect some jobs to remain virtual post-pandemic, leading to permanent changes in the amount of real estate needed for healthcare delivery. The need for a smaller real estate footprint could reduce capital expenditures and costs for hospitals and healthcare systems in the long term.

Consolidation is Coming. COVID-19-induced financial pressures will quickly reveal winners and losers and force further consolidation in the healthcare industry. “Resilient” healthcare systems are likely to be those with a 6% to 8% operating margins, providing the financial cushion necessary to innovate and reimagine healthcare post-pandemic.

Policy Will Get More Thoughtful and Data-Driven. COVID-19 reopening plans will force policymakers to craft thoughtful, data-driven approaches that will necessitate engagement with health system leaders. Such collaborations will be important not only during this current crisis, but also will provide a blueprint for policy coordination during any future pandemic.

As Burik and Fisher point out, hospitals and healthcare systems emerged from previous economic downturns mostly unscathed. However, the COVID-19 pandemic has proven the exception, leaving providers and health systems facing long-term decreases in commercial payments, while facing increased spending to bolster caregiver- and consumer-facing engagement.

“While situations may differ by market, it’s clear that the pre-pandemic status quo won’t work for most hospitals or health systems,” they wrote.

The message for clinical laboratory managers and surgical pathologists is clear. Patients may be permanently changing their decision-making process when considering elective surgery and selecting a provider, which will alter provider test ordering and lab revenues. Independent clinical laboratories, as well as medical labs operated by hospitals and health systems, must be prepared for the financial stresses that are likely coming.