Occupancy rates at skilled nursing facilities remain well below pre-pandemic levels, a trend that weakens the financial health of nursing homes and means fewer test referrals to clinical laboratories that service them

COVID-19 is taking a financial bite out of the nursing home industry as seniors opt for home care rather than entering nursing facilities. If this trend becomes permanent, clinical laboratories may have to ramp up their ability to collect specimens from a growing population of patients who choose non-traditional healthcare settings. And as the SARS-CoV-2 pandemic stretches on, the exodus of seniors from nursing home facilities provides another example of how COVID-19 is altering consumers’ access to healthcare.

According to the most recent “AARP Nursing Home COVID-19 Dashboard Fact Sheets,” the COVID-19 pandemic “has swept the nation, killing more than 160,000 residents and staff of nursing homes and other long-term care facilities.”

Because COVID-19 has hit nursing home residents the hardest, many families have decided elderly parents may be safer living with relatives than in nursing homes that have proven vulnerable to widespread outbreaks. In addition, COVID-19-related lockdowns in skilled nursing facilities (SNFs) have provided families with additional motivation to choose home care for elderly relatives.

For example, in “Should You Bring Mom Home from Assisted Living During the Pandemic?” retired Seattle physician Alison Webb, MD, told Kaiser Health News (KHN) she moved her 81-year-old father, who has moderate dementia, out of assisted living so he could be with grandchildren and enjoy gardening rather than remain in his senior facility, where COVID-19 protocols kept him sequestered from friends and family.

This is not an isolated example and may have a long-term impact on clinical laboratories that service skilled nursing facilities.

Patient Volume Falls Dramatically at Skilled Nursing Facilities

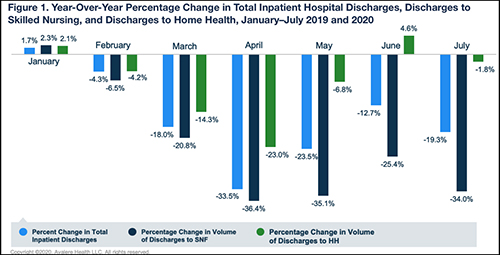

While hospital discharge rates are rebounding to near pre-pandemic levels, an Avalere Health analysis of Medicare fee-for-service claims found a “more drastic and lasting decline in patient volume” at skilled nursing facilities. In contrast, Avalere found home health has experienced a rebound in patient numbers beginning last May.

“In the early months of the COVID-19 outbreak in the US, we saw a substantial decrease in hospital discharges to both skilled nursing facilities and home health agencies,” said Heather Flynn, Consultant at Avalere, in an Avalere press release. “Hospital discharges are steadily moving back to pre-pandemic levels, but our analysis points to an uneven ‘return to normal’ across care settings.”

The graph above, taken from the Avalere press release, reveals “a stark decline in inpatient hospital discharges and discharges to both SNF and home health beginning in February 2020. The analysis further indicated that the skilled nursing industry has experienced a more drastic and lasting decline in patient volume relative to total hospital volume and discharges to home health (where rebounds were observed beginning in May). Of note, discharges to home health experienced a year-over-year increase in June 2020, at 4.6% greater discharge volume when compared to June 2019, while discharges to SNF remained notably below pre-pandemic levels at a 25.4% decrease in year-over-year discharges.” (Graphic copyright: Avalere Health.)

“Skilled nursing facility occupancy typically slows in April after an uptick during the flu season, but we haven’t seen anything like this in recent memory,” Kauffman said in an NIC press release which announced nursing home occupancy had dropped to 78.9% last April, 2020, down 5.5% from 2019. “The long-term effect of COVID-19 on skilled nursing occupancy remains to be seen as the industry adjusts to a new normal.”

Since then, the occupancy rate in skilled nursing properties has fallen even further. The latest Skilled Nursing Monthly Report announced a new low of 74.2%.

Will Clinical Laboratories That Service Skilled Nursing Homes Be Affected?

Mark Parkinson (above), President and CEO of the AHCA and former Governor of Kansas, maintains a successful COVID-19 vaccination rollout and lifting of nursing home visitation bans are keys to the industry’s recovery. “I think the census needs to recover about 1% a month. If we can recover 1% a month on a steady basis, that gets us to the end of 2021,” Parkinson told Skilled Nursing News. “And we’re still down, but we’re down 5% or 6%; we’re not down 13% or 14%. If we recover a half a percent, some businesses will be okay, but not all. If we only recover half a percent, we don’t get any more money, folks are going to have problems. If we don’t have any recovery on census … things are very, very bad.” (Photo copyright: Kansas Health Institute.)

There are signs the nursing home industry may have to contend with home healthcare becoming a permanent competitor for patients. In a news release last spring, the Mayo Clinic announced it was partnering with Medically Home of Boston to launch a virtual hospital-at-home model aimed at delivering “advanced care” from a network of paramedics, nurses, and support team in a home care setting.

The initiative means patients can receive a range of healthcare services in their homes that traditionally required a hospital setting. The services include:

Infusions,

Skilled nursing,

Clinical laboratory and imaging services,

Behavioral health and rehabilitation services.

While the initial program rollout will allow Mayo Clinic to free up ventilators and hospital space for COVID-19 patients, John Halamka, MD, an emergency medicine physician and President of Mayo Clinic Platform, told Modern Healthcare, “Next, we’ll look to forward-thinking organizations who believe like we do in that care should be more convenient and accessible.”

Discharge Doctors Now Choose Home Healthcare Over Skilled Nursing Facilities

Physicians also are embracing home care in greater numbers. As reported in Forbes, a 2020 William Blair survey showed 81% of physicians responsible for discharge planning would send patients to a home health agency rather than a skilled nursing facility. Pre-pandemic, only 54% of discharging physicians expressed a preference for home care, according to the survey.

Greg Chittim, Partner at Health Advances, an international strategy consulting firm headquartered in Boston, points to improvements in virtual technologies as the catalyst for home care’s growth.

“One of the silver linings of COVID-19 is the level of investment we are seeing in virtual care technologies,” Chittim told Forbes. “And beyond the technologies, providers and patients are building that comfort with traditional real-time communication. I think we have moved 10 years ahead in 10 months.”

As the COVID-19 pandemic rolls on and home health initiatives become more commonplace and grow in popularity, clinical laboratory managers may want to develop solutions that assist home healthcare providers with collecting and shipping patient specimens for testing.

While consolidation is a common trend across many sectors—including anatomic pathology groups and hospital systems—UnitedHealth Group is the latest example of the payer-provider consolidation trend impacting medical laboratories nationwide

Pending the successful completion of a $4.9-billion acquisition of DaVita Medical Group, UnitedHealth Group (UNH) will be poised to become the largest single employer of doctors in the U.S., according to numbers reported by leading sources.

Clinical laboratories, anatomic pathology groups, and other service providers that service those doctors should already be taking a serious look at their revenue flows and efficiencies to maintain margins and weather the shift into a model of value-based reimbursement.

Controlling Costs with Direct Care

According to a press release, UnitedHealth Group’s (NYSE:UNH) direct-to-patient healthcare subsidiary, OptumCare, currently employs or is affiliated with 30,000 physicians. And, DaVita Medical Group, a subsidiary of DaVita Inc. (NYSA:DVA), lists 13,000 affiliated physicians on their website. Should acquisition of DaVita Medical Group go forward, OptumCare would have approximately 43,000 affiliated or employed physicians—roughly 5,000 more physicians than HCA Healthcare and nearly double Kaiser Permanente’s 22,080 physicians—thus, making OptumCare’s parent company UNH the largest individual employer of physicians in the U.S. The acquisition is reportedly to reinforce UNH’s ability to control costs and manage the care experience by acquiring office-based physicians to provide services.

OptumCare has seen significant growth over the past decade. OptumHealth, one of three segments of UNH’s overall Optum healthcare subsidiary, includes OptumCare medical groups and IPAs, MedExpress urgent care, Surgical Care Affiliates ambulatory surgery centers, HouseCalls home visits, behavioral health, care management, and Rally Health wellness and digital consumer engagement.

“We have been slowly, steadily, methodically aligning and partnering with phenomenal medical groups who choose to join us,” Andrew Hayek, CEO of OptumHealth (above), told Bloomberg. “The shift towards value-based care and enabling medical groups to make that transition to value-based care is an important trend.” (Photo copyright: Becker’s ASC Review.)

Acquisitions of Doctors on the Rise; Clinical Lab Revenues Threatened

Independent physicians and practices have been a hot commodity in recent years. A March 2018 study from Avalere Health in collaboration with the Physicians Advocacy Institute (PAI) showed that the number of physicians employed by hospitals rose from 26% in July 2012 to 42% in 2016—a rise of 16% over four years.

By acquiring physicians of their own, insurance companies like UnitedHealth Group believe they can offset the cost and shifts in service of these prior trends. “We’re in an arms race with hospital systems,” John Gorman of Gorman Health Group told Bloomberg. “The goal is to better control the means of production in their key markets.”

According to Modern Healthcare, the acquisition of DaVita Medical Group is UnitedHealth’s third such acquisition in 2017. Other acquisitions include:

Advisory Board, a healthcare consulting firm, for $2.3-billion in November.

Along with Surgical Care Affiliates came a chain of surgery centers that, according to The New York Times (NYT), OptumCare plans to use to perform approximately one million surgeries and other outpatient procedures this year alone, while reducing expenses for outpatient surgeries by more than 50%.

NYT also noted that acquisition of DaVita Medical Group doesn’t bring just physicians under the OptumCare umbrella, but also nearly 250 MedExpress urgent care locations across the country.

By having physicians, clinical laboratories, outpatient surgery centers, and urgent care centers within their own networks, insurance providers then can steer patients toward the lowest-cost options within their networks and away from more expensive hospitals. This could mean less demand on independent clinical laboratories and hospitals and, with that, reduced cash flows.

According to NYT, Optum currently works with more than 80 health plans. However, mergers such these—including those between CVS Health (NYSE:CVS) and Aetna (NYSE:AET), and the proposed agreement between Humana (NYSE:HUM) and Walmart (NYSE:WMT) to deliver healthcare in the retailers’ stores—indicate that insurers are seeking ways to offer care in locations consumers find most accessible, while also working to exert influence on who patients seek out, to generate cost advantages for the insurers.

This consolidation should concern hospitals as payers increasingly draw physicians from them, potentially also taking away their patients. The impact, however, may also reach independent medical laboratories, medical imaging centers, anatomic pathology groups, and other healthcare service providers that provide diagnoses and treatments in today’s complex healthcare system.

Deep Payer Pockets Mean Fewer Patients for Clinical Labs and Medical Groups

As this trend continues, it could gain momentum and potentially funnel more patients toward similar setups. Major corporations have deeper pockets to advertise their physicians, medical laboratories, and other service providers—or to raise public awareness and improve reputations. Such support might be harder to justify for independent healthcare providers and medical facilities with shrinking budgets and margins in the face of healthcare reform.

Shawn Purifoy, MD, a family medicine practitioner in Malvern, Ark., expressed his concern succinctly in The New York Times. “I can’t advertise on NBC [but] CVS can,” he noted.

While further consolidation within independent clinical laboratories and hospitals might help to fend off this latest trend, it remains essential that medical laboratories and other service providers continue to optimize efficiency and educate both physicians and payers on the value of their services—particularly those services offered at higher margins or common to menus across a range of service providers.

Often when a hospital health system buys an independent physicians’ practice, the new owner would like its clinical laboratory to serve that medical group

After a hospital or health system buys a physicians’ practice, it is common that the new owner has its in-house medical laboratory provide lab testing to the newly-acquired medical group. Such a purchase is generally good for hospital labs, but not so good for any independent lab that, prior to the sale, had been serving the newly-sold medical practice.

Therefore, when hospitals purchase thousands of physician practices, the impact on the nation’s independent clinical laboratories has the potential to be significant. That’s one conclusion contained in a newly updated report based on co-research by Physicians Advocacy Institute (PAI) and Avalere Health, a healthcare and life sciences consulting firm headquartered in Washington, D.C.

Clinical Laboratory Test Orders Drop as Physicians Join Hospital Staff

According to a PAI news release, hospitals acquired 5,000 independent physician practices between July 2015 and July 2016. Building on a previous Avalere-PAI study, the data suggest that over four years (from mid-2012 to mid-2016) the percentage of hospital-employed physicians increased by more than 63%. In other words, 42% of doctors were employed by hospitals in July 2016, as compared to 25% of doctors in July 2012, a proportion that nearly doubled in just four years!

As more physicians move from owning their private practice to becoming employees of the new owner, independent labs serving those medical practices are at risk of losing the lab test referrals from the practice.

Of course, this can be a boon for hospital-based or healthcare system labs that see an uptick in lab test referrals, as more physician practices or outreach customers join the hospital team. However, surveys show, for hospitals, acquiring and owning more doctors’ practices can be problematic.

“As payers and hospitals continue [to] drive consolidation across the healthcare system, it is becoming more and more difficult for a physician to maintain an independent practice,” stated Robert Seligson (above), PAI President and CEO of the North Carolina Medical Society, in the PAI news release. “Payment policies mandated by insurers and [the] government heavily favor large health systems, creating a competitive advantage that stacks the deck against independent physicians, who are already struggling to survive under expensive, time-consuming administrative and regulatory burdens.” (Photo copyright: Physicians Advocacy Institute.)

The newest data, released by PAI in 2018, suggest that from July 2015 to July 2016 hospitals were actively buying physician practices:

5,000 physician practices were acquired by hospitals;

8% to 47% growth in hospital-owned practices in every region of the U.S.; and,

More than 33% of Midwest physician practices were hospital-owned in 2016.

The data also indicated that more doctors had chosen to become employed by healthcare systems, giving up their independent status. From mid-2015 to mid-2016:

14,000 more physicians became hospital employees;

11% increase in employed physicians; and

5% to 22% growth of hospital-employed doctors in every U.S. region, with more than 50% in the Midwest, 37% in the south, and 33% in Alaska and Hawaii.

“Physician compensation is one of the fastest growing expenses in health systems. It has become as high as 10% of total expenses for some systems. The burden is not sustainable,” Joel French, Chief Executive Officer, SCI Solutions, told Modern Healthcare.

Medicare Pays More to Hospitals for the Same Services

The PAI-Avalere report also noted that Medicare pays more for certain services when performed in hospital outpatient departments instead of doctors’ offices.

$5,148 for hospital cardiac imaging compared to $2,862 in a doctor’s office;

$1,784 for a colonoscopy in-hospital versus $1,322 in a physician’s office; and,

$525 for in-hospital evaluation and management services compared to $406 in the doctor’s office.

“The shift toward more physicians employed by hospitals could mean higher costs for the entire healthcare system,” Kelly Kenney, PAI Executive Vice President, stated in the PAI news release.

Practice Ownership Effects Quality of Care

While the PAI-Avalere analysis explored physician employment’s impact on payment for some services, another study explored its effects on quality of care.

Researchers analyzed data from three national surveys of physician practices. Their report, published in the American Journal of Managed Care (AJMC), found that in hospital-owned physician practices, there was more use of recommended care management processes (CMPs), such as, disease registries and nurse coordinators.

“The current findings suggest that hospital acquisition of practices may have beneficial effects for patients with chronic illnesses,” the researchers wrote in AJMC.

As medical groups change owners, independent clinical laboratories must work hard to retain the testing business—especially when the new owner is a hospital or healthcare system with its own in-hospital medical laboratories.

Aetna’s CEO Mark Bertolini highlights how the current system increases costs for both insurers and consumers

At the moment, probably no issue is more politicized than that of the Affordable Care Act (ACA), often called Obamacare. Because it controls the design of health insurance coverage, it also influences the way health plans pay hospitals, physicians, clinical laboratories, and anatomic pathology groups.

However, understanding the truth about what is working and what is not with the Affordable Care Act is a complex undertaking. That is because both the advocates and critics of this law are engaged in highly-partisan rhetoric, despite the fact that most have no intimate knowledge of how healthcare works in the United States. (more…)

Health insurers offering Medicare Advantage plans are narrowing their networks and favoring the national clinical lab companies over local medical labs and pathology groups

Enrollment in Medicare Advantage health plans is booming. This development is not auspicious for local medical laboratories, hospital lab outreach programs, and anatomic pathology groups because the private health insurers operating these plans typically prefer to contract with national lab companies while narrowing their lab networks.

The mathematics of this trend are simple. As Medicare Advantage enrollment increases, the proportion of patients covered by traditional Medicare Part B fee-for-service shrinks. The consequence is that local labs have fewer Medicare Part B patients to serve and are locked out of providing medical laboratory testing services to Medicare Advantage patients. (more…)